Boyar's Research Digest #25

January 14th, 2024

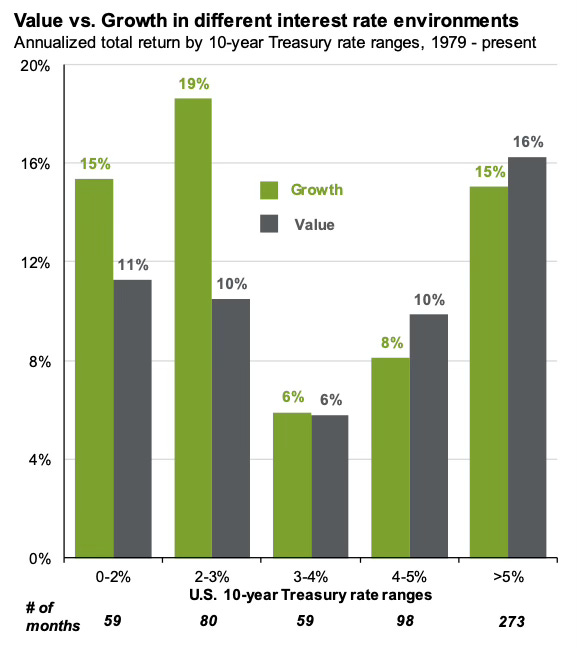

Growth vs. Value in Different Interest Rate Environments

Most consumers are well-aware of the effect that interest rates—both short- and long-term—can have on their expenses. Consumers with credit card debt pay interest based on where short-term interest rates are (plus other factors including an individual’s credit score). Yields on 30-year mortgages—the preferred mortgage product of almost 90% of U.S. homebuyers—loosely track the path of 10-year U.S. Treasury rates.

But some investors may not be as well-versed in how interest rates affect stocks, particularly when weighing the differences between value and growth equities. Generally speaking, growth stocks perform relatively better in low interest rate environments, while value shares often lead when 10-year Treasury rates are 4% or higher. Between 3%-4%, history shows, is where the equation roughly balances out between growth and value shares.

This interest rate effect on value vs. growth stocks makes logical sense: When rates are low, earlier-stage/expanding companies are more willing and able to tap credit markets to facilitate their growth. Conversely, when interest rates are higher, the capital that many growing companies rely upon (including those that are not yet profitable) to fund their expansion becomes more costly. Furthermore, the price investors are willing to pay for growth stocks tends to be sensitive to expectations of cash flows well into the future, which become more significantly discounted in higher interest-rate backdrops.

In response to elevated—and not so transient—inflation, the Federal Reserve’s aggressive rate hiking cycle that started in March 2022, with 11 hikes ranging from 25bps to 75bps each, bringing the fed funds rates from 0.25% to 5.5% in less than 1 ½ years—the fastest rate hiking cycle since the 1980s. During this span, the 10-year yield surged from under 2.5%, briefly jumping above 5.0% last October. Since then, however, the 10-year underwent a sudden retracement, as the Fed has paused hiking interest rates, and expectations have shifted to interest rate cuts on the horizon in 2024.

We find it unlikely that the Fed will go back to periods of ultra-low rates like we experienced since the end of the Great Financial Crisis and during the COVID-19 pandemic. The current consensus among most Fed officials is that short-term rates will likely close out 2024 in a 4.5%-5.0% range, and none of the Fed officials foresees short-term rates going much below 2.5% even over the longer run. Meanwhile, the normalization of 10-year yields above 3% (currently ~4.0%) seems to suggest that—in contrary to a long period of growth outperforming value between the Great Financial Crisis and the COVID-19 pandemic while rates were historically low—value shares may be primed for a durable resurgence.

In other news:

Join us Tuesday as Jonathan Boyar sits down with Barron’s Editors Lauren Rubin and Ben Levisohn. Register with Barrons to attend the webinar.

In case you missed it:

Jonathan Boyar joined Clay Fink on his podcast “We Study Billionaires” for a discussion on Uber, Howard Hughes, and other stocks he finds compelling.

Comin up:

January’s Opportunity Report is going through a few finishing touches and should be ready for your inbox by the close of next week. In the mean time, don’t miss December’s issue if you haven’t read it yet.

Thanks for reading, and enjoy the rest of your weekend!

—Boyar Research

Important Disclosures. The information herein is provided by Boyar’s Intrinsic Value Research LLC (“Boyar Research”) and: (a) is for general, informational purposes only; (b) is not tailored to the specific investment needs of any specific person or entity; and (c) should not be construed as investment advice. Boyar Research does not offer investment advisory services and is not an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) or any other regulatory body. Any opinions expressed herein represent current opinions of Boyar Research only, and no representation is made with respect to the accuracy, completeness or timeliness of the information herein. Boyar Research assumes no obligation to update or revise such information. In addition, certain information herein has been provided by and/or is based on third party sources, and, although Boyar Research believes this information to be reliable, Boyar Research has not independently verified such information and is not responsible for third-party errors. You should not assume that any investment discussed herein will be profitable or that any investment decisions in the future will be profitable. Investing in securities involves risk, including the possible loss of principal.

Important Information: Performance Information. Past performance does not guarantee future results. The reports in this sample are for informational purposes only and the performance of the stocks selected is not indicative of the performance of all the stocks profiled in Boyar Research. The performance of the stocks selected and the performance of the stocks in Boyar Research may in fact diverge materially. Additional information regarding the performance of other companies featured in Boyar Research is available from Boyar Research upon request. This information is not a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, including an interest in any investment vehicle managed or advised by affiliates of Boyar Research. Any information that may be considered advice concerning a federal tax issue is not intended to be used, and cannot be used, for the purposes of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter discussed herein. Clients of an affiliate of Boyar Research and employees of Boyar Research own shares in Uber and Howard Hughes Corporation.