Markel: Boyar's 2023 Forgotten Forty + Updated Thoughts

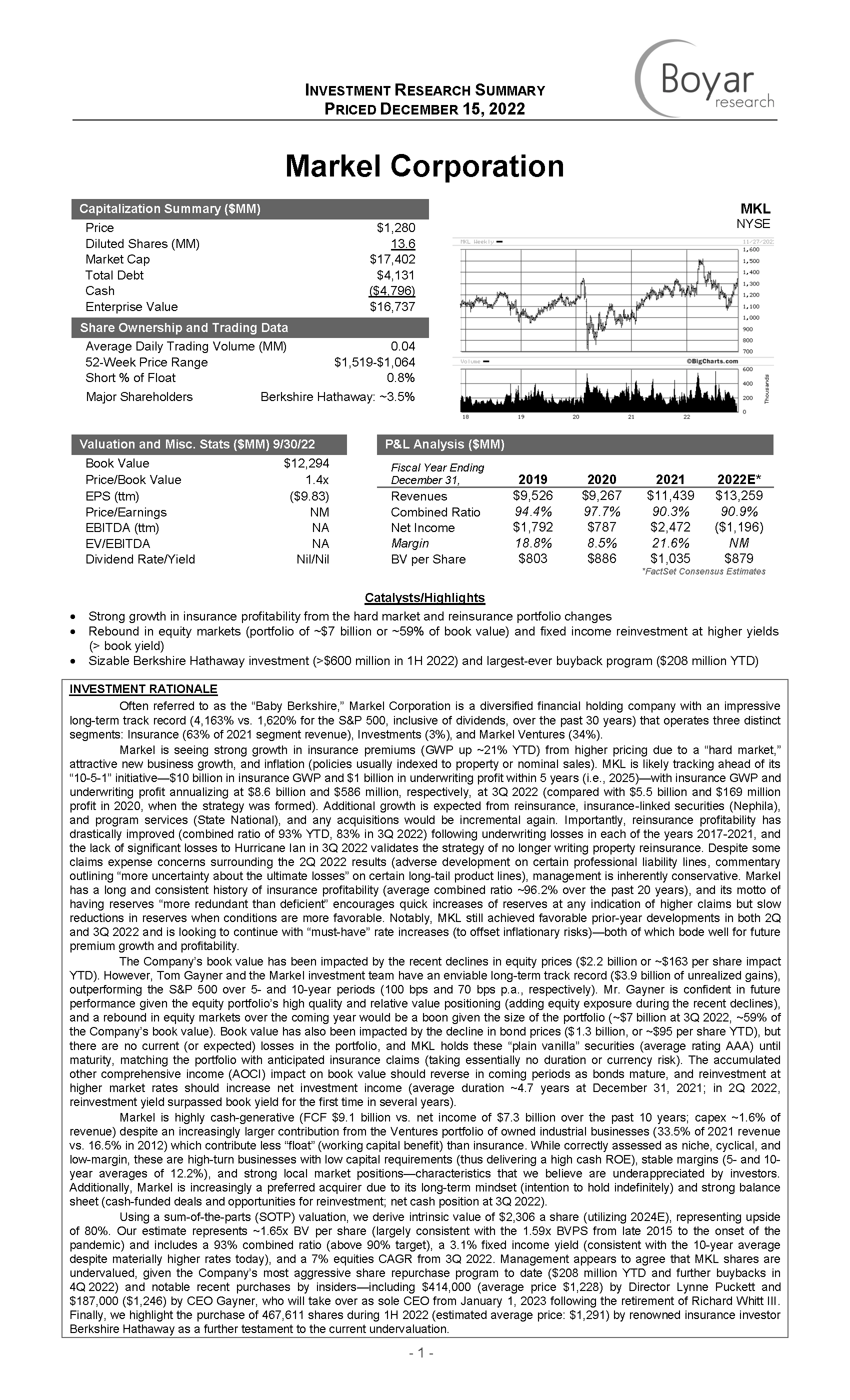

Markel (MKL)

Markel (MKL)

Ventures (MKL’s privately owned business portfolio) has delivered record results in 2023. No further acquisitions have followed the 2022 purchase of Metromont, but Markel looks well placed to resume dealmaking given competitors’ higher funding costs and the strength of its own balance sheet (~$2.8 billion in net cash). Investment income is rising rapidly, being up 9.3% YoY in the first 9 months of 2023—below the S&P return of 13.1% but commendable given MKL’s value-oriented approach and lower exposure to the “Magnificent 7.”

Unfortunately, insurance profitability deteriorated in 3Q 2023 (99% combined ratio vs. 93% in 1H), and growth also slowed. Fortunately, however, these appear to reflect largely temporary issues (e.g., challenges in a new IP collateral protection line, slowdown in capital markets), and both growth and profitability are expected to improve. Management is transparent about the challenges and conservative in estimating loss costs and is focusing on holding reserves that are “more likely to prove redundant than deficient”—all while executing the most aggressive share repurchase program to date ($270 million YTD, following $497 million in 2021-2022) alongside heavy insider buying (~$2.2 million in repurchases by eight insiders since May 2022, including $325,000 by four directors after the 3Q 2023 results).

For more information on the Forgotten Forty, email via Substack or at info@boyarvaluegroup.com.

Important Disclosures. The information herein is provided by Boyar’s Intrinsic Value Research LLC (“Boyar Research”) and: (a) is for general, informational purposes only; (b) is not tailored to the specific investment needs of any specific person or entity; and (c) should not be construed as investment advice. Boyar Research does not offer investment advisory services and is not an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) or any other regulatory body. Any opinions expressed herein represent current opinions of Boyar Research only, and no representation is made with respect to the accuracy, completeness or timeliness of the information herein. Boyar Research assumes no obligation to update or revise such information. In addition, certain information herein has been provided by and/or is based on third party sources, and, although Boyar Research believes this information to be reliable, Boyar Research has not independently verified such information and is not responsible for third-party errors. You should not assume that any investment discussed herein will be profitable or that any investment decisions in the future will be profitable. Investing in securities involves risk, including the possible loss of principal.

Important Information: Performance Information. Past performance does not guarantee future results. The reports in this sample are for informational purposes only and the performance of the stocks selected is not indicative of the performance of the entire Forgotten Forty. The performance of the stocks selected and the performance of the Forgotten Forty may in fact diverge materially. Additional information regarding the performance of other companies in the Forgotten Forty is available from Boyar Research upon request. This information is not a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, including an interest in any investment vehicle managed or advised by affiliates of Boyar Research. Any information that may be considered advice concerning a federal tax issue is not intended to be used, and cannot be used, for the purposes of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter discussed herein. Clients of an affiliate of Boyar Research and employees of Boyar Research own shares in MKL.