Opportunity: February 2025

On a Journey from Good to Great.

Introduction

It has been a tumultuous few years for the Company featured in this month’s Opportunity Report, but we believe that it remains firmly on the path “from good to great” that began with its IPO just over 10 years ago. Management has greatly improved all aspects of its business model, including its product offerings, its cost base, and the quality of its customers, yet many investors seem to be slow in appreciating the dramatic changes of the past decade. The Company also has a unique opportunity to gain market share following the failure of one of its competitors during the industry fallout in 2023, and the reversal of a mistake by management the year before is set to provide a huge tailwind to earnings over the next 2-3 years.

Is it time to bank on Citizens Financial Group (ticker: CFG)?

Citizens Financial Group

NYSE: CFG

Key Highlights

Citizens’ management has greatly improved the quality of its banking franchise since the Company’s IPO in 2014, enhancing its product suite, geographic coverage, and customer base.

In 3Q 2022, the management team initiated an interest rate hedging program to make the Bank’s future earnings more stable and predictable. This is depressing the Bank’s current earnings but is set to completely unwind by 2027, adding more than $500 million in annual net income.

The failure of First Republic Bank in 2023 has created a unique opportunity for Citizens to expand its wealth management business. It launched a private bank in September 2023 that is expected to add 5% to EPS in 2025, with a return on tangible common equity (ROTCE) of 20%-24% over the medium term.

Citizens’ earnings per share are set to rise significantly over the next 3 years, with management targeting $6.40 by 2027, or more than 110% over 2024 levels. We are slightly more cautious than both management and consensus (which expects $6.13) but still see significant upside, estimating an intrinsic value of $65 in 2027 or 45% above the current share price. This is based on an EPS of $5.43 and a P/E multiple of 12x, consistent with the Company’s average since its IPO. Investors are also set to receive a dividend of $1.68 per year, for a yield of 3.7%, providing an extra boost to an already attractive return outlook.

History

The Company’s history dates back to High Street Bank, which was founded in Rhode Island in 1828 and eventually formed Citizens Savings Bank in 1871. More relevant to our investment thesis, in 1988 Citizens was acquired by The Royal Bank of Scotland (RBS, now known as Natwest Group). This turned out to be an era of aggressive acquisitions for RBS, which briefly became the largest bank in the world, with a balance sheet the size of the German economy. However, like many companies before it, its excessive M&A activity ultimately led to its downfall. The infamous takeover of Dutch bank ABN Amro in 2007 (the largest transaction in the history of financial services) proved to be “the beginning of the end,” and in the global financial crisis that followed, the British government had to inject a GBP 45.5 billion bailout in return for an 80% stake in the bank. RBS then underwent a period of severe restructuring, part of which involved selling Citizens via an IPO on the NYSE on September 23, 2014.

Since Citizens’ IPO, management has greatly improved the quality of its banking franchise. It has fully revamped its commercial product offering (adding escrow, insolvency/bankruptcy, and treasury services), added a digital self-service platform for small business and lower-middle-market customers, redeveloped its payments business, and, on the consumer side, succeeded in attracting an affluent and tech-savvy customer base. It has also increased its scale and presence in new markets through the acquisition of HSBC’s East Coast branches and Investors Bancorp based in New Jersey, built out its investment banking capabilities through a series of acquisitions (including JMP Capital, Willamette, and DH Capital), and expanded into new higher-growth geographies (such as Texas and Florida), and now it is building out a private bank with a wealth management offering focused on high-net-worth and ultra-high-net-worth customers. As the Company’s profitability has drastically improved, shareholders have begun to reap the benefits, including through increased dividend payments, but we believe that plenty of opportunity remains as management implements its goal of becoming a high-performing regional bank.

Citizens Financial Group Historical Earnings Per Share and Dividends Per Share

Business Overview

Citizens Financial Group is headquartered in Providence, RI, and is the 17th-largest commercial bank holding company in the U.S., measured by total assets. As of December 31, 2024, its balance sheet held $218 billion in assets (including $139 billion in loans), $175 billion in deposits, and $24.3 billion in stockholders’ equity.

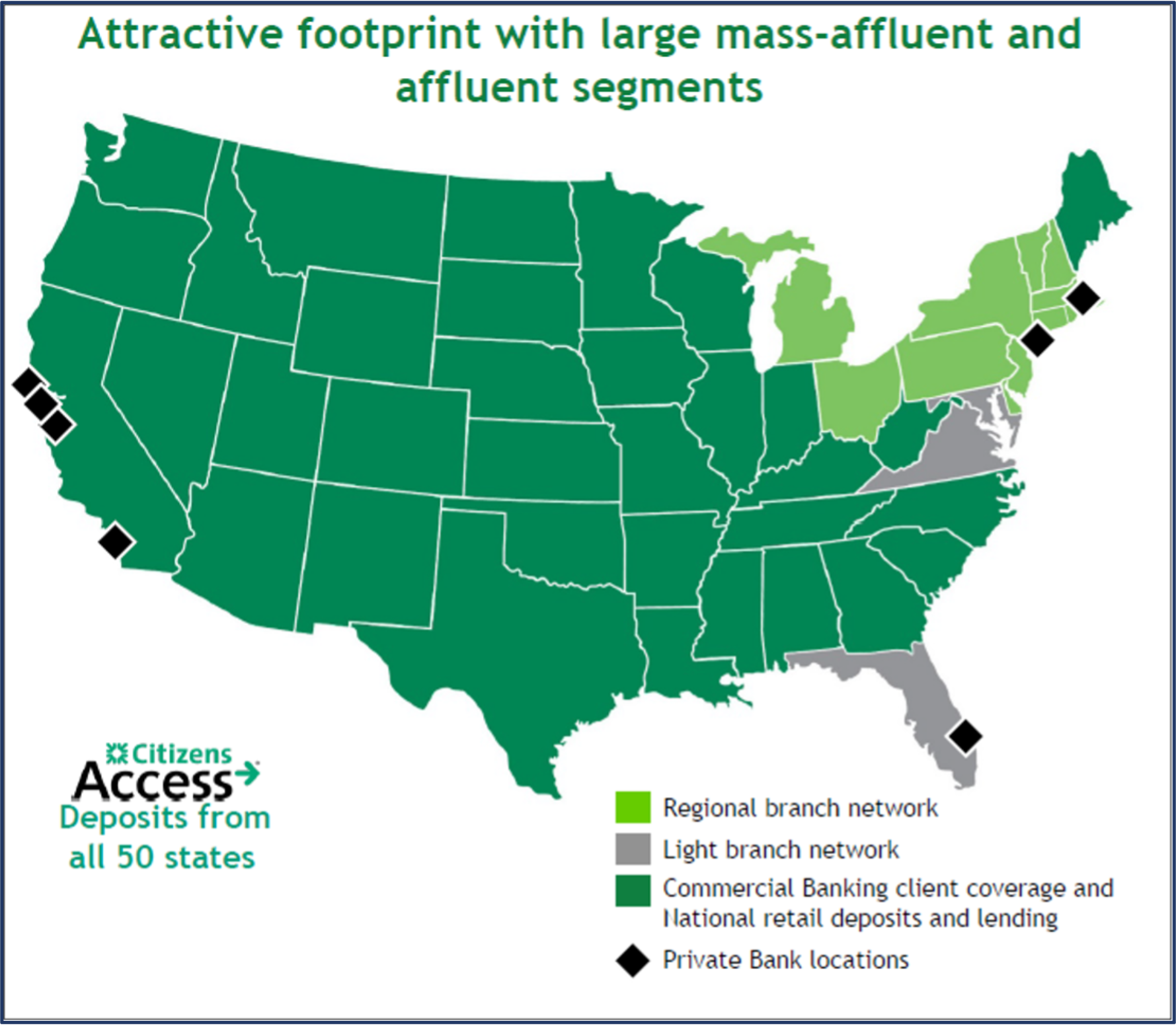

Citizens serves more than 6 million customers via 1,000 branches and 3,100 ATMs in a 14-state footprint covering the New England, Mid-Atlantic, and Midwest regions (along with the District of Columbia); offers a nationwide digital banking platform; and serves retail and commercial customers via 105 retail and commercial offices across all 50 states.

The Company holds a top 5 market share position of deposits in 6 of its 10 most prominent metropolitan statistical areas (MSAs), which have diverse economies and affluent demographics, and in its most important markets, Boston and Philadelphia, it has leading commercial banking positions. It has also gained a larger foothold in the enormous New York-Newark-New Jersey MSA as a result of the acquisitions of the HSBC branches in 2021 and Investor Bancorp (ISBC) in 2022.

Citizens Financial Group Branch Footprint and Service Coverage

In 2024, Citizens generated $7.8 billion in revenues and $3.03 in EPS across two primary business segments:

Consumer Banking (67% of 2024 revenue) serves consumer customers and small businesses that have annual revenues up to $25 million with a variety of lending (mortgage, home equity lending, credit cards, small business loans, wealth management, investments services) and depository products across its traditional banking footprint, as well as education and point-of-sale finance loans (i.e., Citizens Pay) and digital deposit products (i.e., Citizens Access) nationwide.

Commercial Banking (33% of 2024 revenue) serves companies and institutions that have annual revenues typically ranging from $25 million to >$3 billion with a variety of financial products, including lending and leasing, depository and treasury management services, foreign exchange, and interest rate and commodity risk management solutions, as well as syndicated loans, corporate finance, mergers and acquisitions, and debt and equity capital markets.

Unwinding of Hedging Misstep to Boost Future Earnings

In 3Q 2022, CFG management initiated an interest rate hedging program to make the Bank’s future earnings more stable and predictable. Citizens is one of the most “asset-sensitive” banks, meaning that its earnings fluctuate more significantly as the Fed funds rate moves up and down. This asset sensitivity reflects the Bank’s high proportion of adjustable-rate loans, which account for more than 60% of total loans (among them commercial and industrial [C&I] loans and home equity loans).

When interest rates increased from the record lows seen in 2022, the interest rates on these variable-rate loans increased immediately while the cost of Citizens deposits used to fund these loans rose more slowly (or not at all, in the case of demand deposit accounts). As a result, management put in place hedges to protect this new level of profitability in case interest rates began to decrease once again. In hindsight, this proved to be a mistake, and Citizens is now receiving a fixed rate of interest from the hedges that is significantly below the adjustable rate it would otherwise be receiving from its loan portfolio.

This was an expensive lesson in attempting to time interest rate movements, but fortunately the effects are temporary and will begin to reduce in 2025 before unwinding completely over 2026 and 2027. This reversal is set to be a huge benefit to Citizens’ bottom line, with more than $500 million in additional net income by 2027—a substantial figure considering that Citizens generated $1.5 billion in net income in 2024.

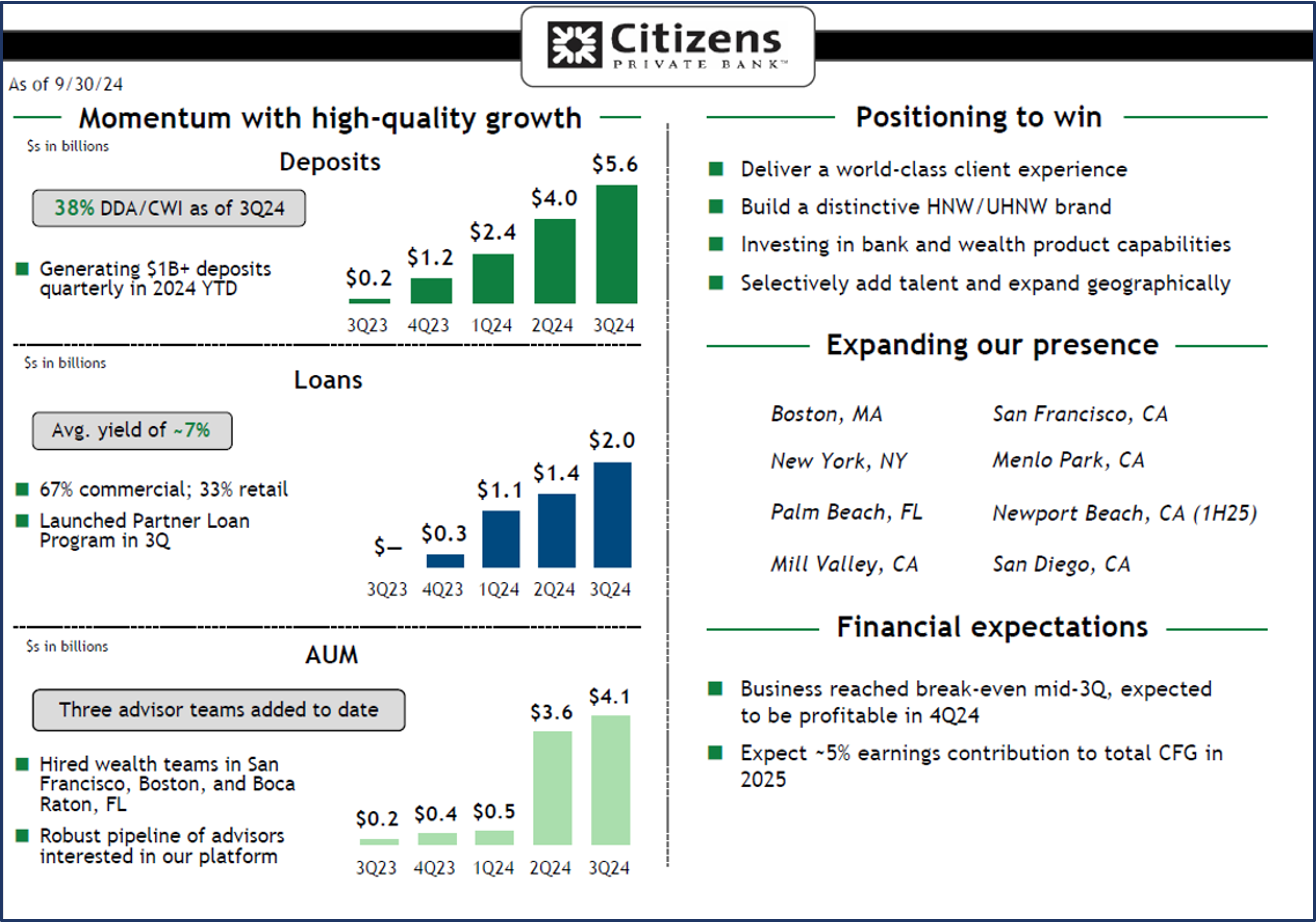

With Failure Comes (a Private Bank) Opportunity

Citizens’ customer base has significant exposure to high-net-worth individuals, and management has long tried to expand its wealth management services with the aim of servicing this clientele with a broader range of products. However, it has continually struggled to find acquisition candidates that meet its financial return targets (except in 2019, when Citizens acquired Clarfeld Financial Advisors, a family office providing investment, financial planning, and tax and estate planning services to high-net-worth and ultra-high-net-worth individuals). In 2023, CEO Bruce van Saun believed that he saw a unique opportunity to acquire the assets of the failed First Republic Bank, but he was ultimately outbid by JPMorganChase.

Instead, Citizens has elected to build out its wealth management capabilities organically as part of a new private bank. Launched in September 2023, Citizens Private Bank offers wealth management, investing, portfolio management, and estate planning to high-net-worth clients with a strong technology focus and white-glove service similar to that of First Republic (although without the extraordinarily favorable lending rates). It was able to kickstart the operations with approximately 50 senior private bankers and related support staff who were formerly employees of First Republic but who defected to CFG rather than take on new positions at JPM.

While Mr. van Saun admits that there is “more to do to get to white-glove service,” the private bank is making strong progress. It hit breakeven in 4Q 2024, on track with management’s original targets, and has already added $7 billion in deposits, $3 billion in loans (with an average interest rate of ~7%), and $4.7 billion in assets under management. Management expects to open four more branches in 2025 (beyond the four already operating), and the private bank is on target to add 5% to Citizens’ EPS in 2025, with a return on tangible common equity of 20%-24% over the medium term.

Citizens Private Bank

Valuation

Citizens shares currently trade at a 2024 P/E multiple of 14.8x. While to some investors this might not scream value for a regional bank, the Bank’s “E” (earnings per share) is set for a significant increase over the next few years. In fact, management has consistently reiterated its target of a 16%-18% return on tangible common equity (ROTCE) over the “medium term” (which it implies is 2027). This would translate to an EPS of greater than $6.40, a whopping increase of more than 110% over the $3.03 seen in 2024 (when the ROTCE was just 9.8%).

While this might seem a tall order, we note that about half this improvement in profitability is due to the reversal of the interest rate hedges, already described. Even so, we are inherently skeptical of multi-year targets set by management and therefore take a slightly more cautious approach, estimating $5.40 in EPS in 2027. Applying a 12x P/E multiple to this estimate (consistent with the Company’s average since its IPO), we estimate an intrinsic value of $65 per share, for 45% upside from current levels. Investors are also set to receive a dividend of $1.68 per year, for a yield of 3.7%, providing an extra boost to an already attractive return outlook.

Boyar’s Final Word

It has been a tumultuous few years in the banking industry, and the macroeconomic outlook remains uncertain. But Citizens has two unique features that are set to drive significant earnings growth over the next several years: the reversal of the ill-timed interest rate hedge put in place in late 2022 and the buildout of its private bank and wealth management capabilities. We believe that Citizens has made substantial progress since its IPO 10 years ago, improving the quality of its franchise, its product suite, and its customer base, yet its current valuation suggests that these improvements and its future earnings potential remain underappreciated by most investors. With a healthy dividend yield of 3.7% and a discounted valuation, and a significant boost to net profit over the next 3 years, we believe that Citizens looks like an interesting opportunity today.

Important Disclosures. The information herein is provided by Boyar’s Intrinsic Value Research LLC (“Boyar Research”) and: (a) is for general, informational purposes only; (b) is not tailored to the specific investment needs of any specific person or entity; and (c) should not be construed as investment advice. Boyar Research does not offer investment advisory services and is not an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) or any other regulatory body. Any opinions expressed herein represent current opinions of Boyar Research only, and no representation is made with respect to the accuracy, completeness or timeliness of the information herein. Boyar Research assumes no obligation to update or revise such information. In addition, certain information herein has been provided by and/or is based on third party sources, and, although Boyar Research believes this information to be reliable, Boyar Research has not independently verified such information and is not responsible for third-party errors. You should not assume that any investment discussed herein will be profitable or that any investment decisions in the future will be profitable. Investing in securities involves risk, including the possible loss of principal. Important Information: Past performance does not guarantee future results. The company mentioned in this sample are for informational purposes only and the performance of the stock selected is not indicative of the performance of the stocks profiled in Boyar Research, the performance of the stocks selected, and the performance of Boyar Research may in fact diverge materially. Additional information regarding the performance of other companies in Boyar Research is available upon request.

This information is not a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, including an interest in any investment vehicle managed or advised by affiliates of Boyar Research. Any information that may be considered advice concerning a federal tax issue is not intended to be used, and cannot be used, for the purposes of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter discussed herein. Clients of an affiliate of Boyar Research and employees of Boyar Research own shares in Citizens Financial Group.