Revisiting Medtronic

A look back at 2022's Forgotten Forty

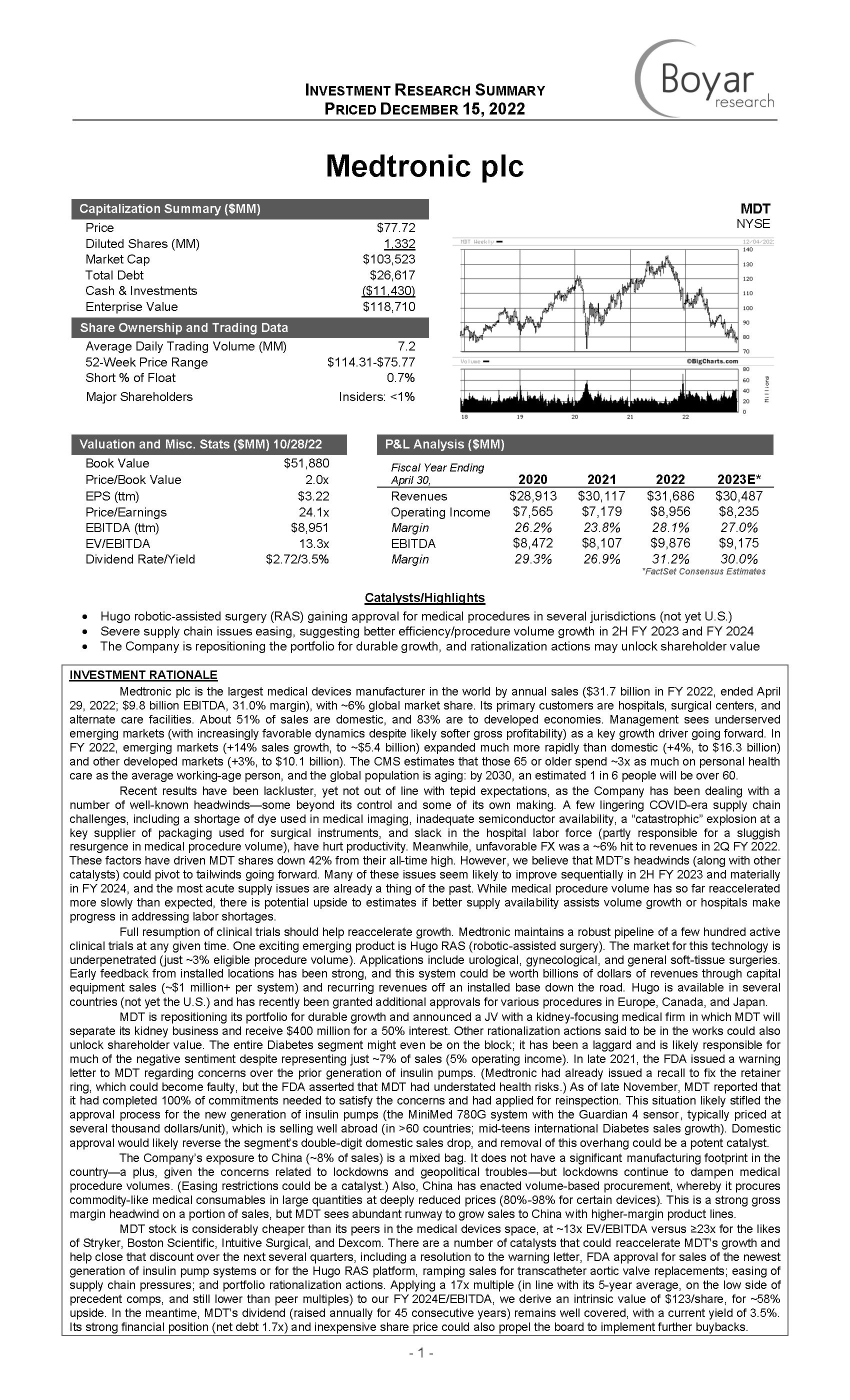

In last year’s Forgotten Forty, we identified medical device maker Medtronic as an attractive investment owing to its numerous identifiable catalysts, prospects for revenue and earnings growth acceleration, and inexpensive valuation relative to its peer group. The share price has tracked a bumpy path over the last 12 months but as of this writing is essentially flat YoY (up 1%) versus a 16% gain for the S&P 500.

Given that we remain in the bull camp for MDT, we clearly still find investment merit in the name. But perhaps what we overestimated was the impact that some of our identified catalysts would have on near-term results and how quickly Medtronic’s bottom-line growth would resume. This year, the Company did, indeed, resolve the issue brought up by the FDA regarding the safety of its previous-generation insulin pump systems and was granted FDA approval to sell the newest generation of products in the U.S. (which were already selling well abroad in >60 countries and generating mid-teens growth). Sales in the U.S. took time to ramp up (the system requires a prescription from a healthcare professional), but the Diabetes segment is now back to mid-single-digit growth (a reversal from down 3% in FY 2023). Yet, with the Diabetes segment comprising just ~7% of overall sales, investors have largely shrugged off the improvement: While the insulin pump concerns were the source of heightened investor scrutiny, removing the overhang seems to have merely halted downward share pressure instead of fostering a turnaround as we had earlier postulated.

We also identified its emerging robotic-assisted surgery platform as a potential catalyst even knowing that the ramp was going to be deliberately slow and measured owing to both tight supply of components (primarily semiconductors) and the Company’s desire to fine tune the product before a wider launch. The system is undergoing clinical trials in the U.S., and while we still expect this to be a significant long-term revenue driver, the timing of regulatory approvals for various surgical procedures remains uncertain.

(Also, what we certainly did not factor into our 1-year outlook at the time was that the hype around GLP-1 drugs would spur widespread speculation that a reduction of obesity prevalence would lead to fewer people with diabetes and fewer cardiovascular surgery procedures—two of Medtronic’s primary markets. We think this concern is far overblown.)

In conclusion, this turnaround story is taking longer than we once thought. Medtronic shares fell >40% in value before being featured in last year’s Forgotten Forty—greatly de-risking the equity, in our view—but have not yet staged a meaningful recovery as earnings growth projections have been pushed out several quarters. However, MDT remains attractively valued, has a strong pipeline of growth opportunities in diabetes, robotic assisted surgery, and renal denervation, and pays a 3.5% yield for investors to wait.

Important Disclosures. The information herein is provided by Boyar’s Intrinsic Value Research LLC (“Boyar Research”) and: (a) is for general, informational purposes only; (b) is not tailored to the specific investment needs of any specific person or entity; and (c) should not be construed as investment advice. Boyar Research does not offer investment advisory services and is not an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) or any other regulatory body. Any opinions expressed herein represent current opinions of Boyar Research only, and no representation is made with respect to the accuracy, completeness or timeliness of the information herein. Boyar Research assumes no obligation to update or revise such information. In addition, certain information herein has been provided by and/or is based on third party sources, and, although Boyar Research believes this information to be reliable, Boyar Research has not independently verified such information and is not responsible for third-party errors. You should not assume that any investment discussed herein will be profitable or that any investment decisions in the future will be profitable. Investing in securities involves risk, including the possible loss of principal. Important Information: Past performance does not guarantee future results. The company mentioned in this sample are for informational purposes only and the performance of the stock selected is not indicative of the performance of the stocks profiled in Boyar Research, the performance of the stocks selected, and the performance of Boyar Research may in fact diverge materially. Additional information regarding the performance of other companies in Boyar Research is available upon request.

This information is not a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, including an interest in any investment vehicle managed or advised by affiliates of Boyar Research. Any information that may be considered advice concerning a federal tax issue is not intended to be used, and cannot be used, for the purposes of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter discussed herein. Clients of an affiliate of Boyar Research and employees of Boyar Research own shares in Medtronic plc.