Historically spinoffs have been a good source of market-beating investment ideas. Conventional wisdom on spinoffs (made popular by investing legend Joel Greenblatt’s well-known investment book You Can Be a Stock Market Genius) says that spun-out entities tend to thrive when given the freedom to focus on their core products and services. At the same time, it’s hard for many investors to recognize the value of a smaller division buried within the complex finances of a large conglomerate. After such an entity gets spun off, investors usually have an easier time valuing it more accurately. As a result, the sum of the parts of an entity ripe for a spinoff can sometimes wind up being worth more than the conglomerate was valued at beforehand. However, investors need to be careful, because not all spinoffs are created equal (more on this later).

“Spinoffs are an interesting place to look because there’s a natural constituency of sellers and there’s not a natural constituency of buyers.”

– Seth Klarman

In 2019, our analyst team noticed something interesting: companies that had been spun off over the prior decade had underperformed the S&P 500 (by ~2.7% per year, on average). So we decided to issue a comprehensive report analyzing this phenomenon. Our deep dive revealed that their lackluster average performance masked some unique opportunities for the discerning investor. Spinoffs that performed well had an average outperformance (i.e., a return greater than the S&P 500) of ~11% from the spinoff date. Our data showed that even if the group as a whole did not perform well, uncovering the best spinoffs can generate truly spectacular returns (although that’s much easier said than done!). This article provides some tips and tricks to help you find such profitable situations.

We wondered why the conventional wisdom on spinoffs hasn’t held—and whether there are still opportunities to be had among newly formed companies. Paid subscribers have full access toread the introduction of our 2019 spinoff report. While our analysis is from 2019 (and largely hasn’t been updated), we believe that our conclusions are still valid, since the factors that drove the underperformance of many spinoffs have not abated (and in some cases have only increased).

As an aside, this Sunday we’ll be releasing a report on a relatively recent spinoff that we believe is ripe for significant capital appreciation.

Our team’s research suggested three elements that have been hurting spinoff transactions in recent years:

The growth of passive investing:

When a company creates a spinoff, investors need to figure out a new market value for both the parent company being left behind and the spinoff company being created. Often investors assign a value to the new company that is much lower than its actual value, and that gap can be a great opportunity for an active manager—but only if the gap closes over time. As investors have moved away from active managers, including hedge funds, those managers have had less capital available to buy shares of spinoffs, which has caused shares to languish.

Source: Morningstar Direct Asset Flows. Data as of July 31, 2023.

As the preceding chart shows, fund flows have not yet reversed in favor of active managers. However, if that trend changes, we could start to see such a shift occur, leaving active managers with more dry powder they can use to invest in undervalued companies, including ignored spinoff issues. In this way an increase in flows to active management could improve the short-term performance of spinoffs.

Increased shareholder activism:

Activist investing has emerged as a legitimate investment strategy that has attracted significant capital, and activist investors have pressured companies to spin off underperforming or weaker divisions.

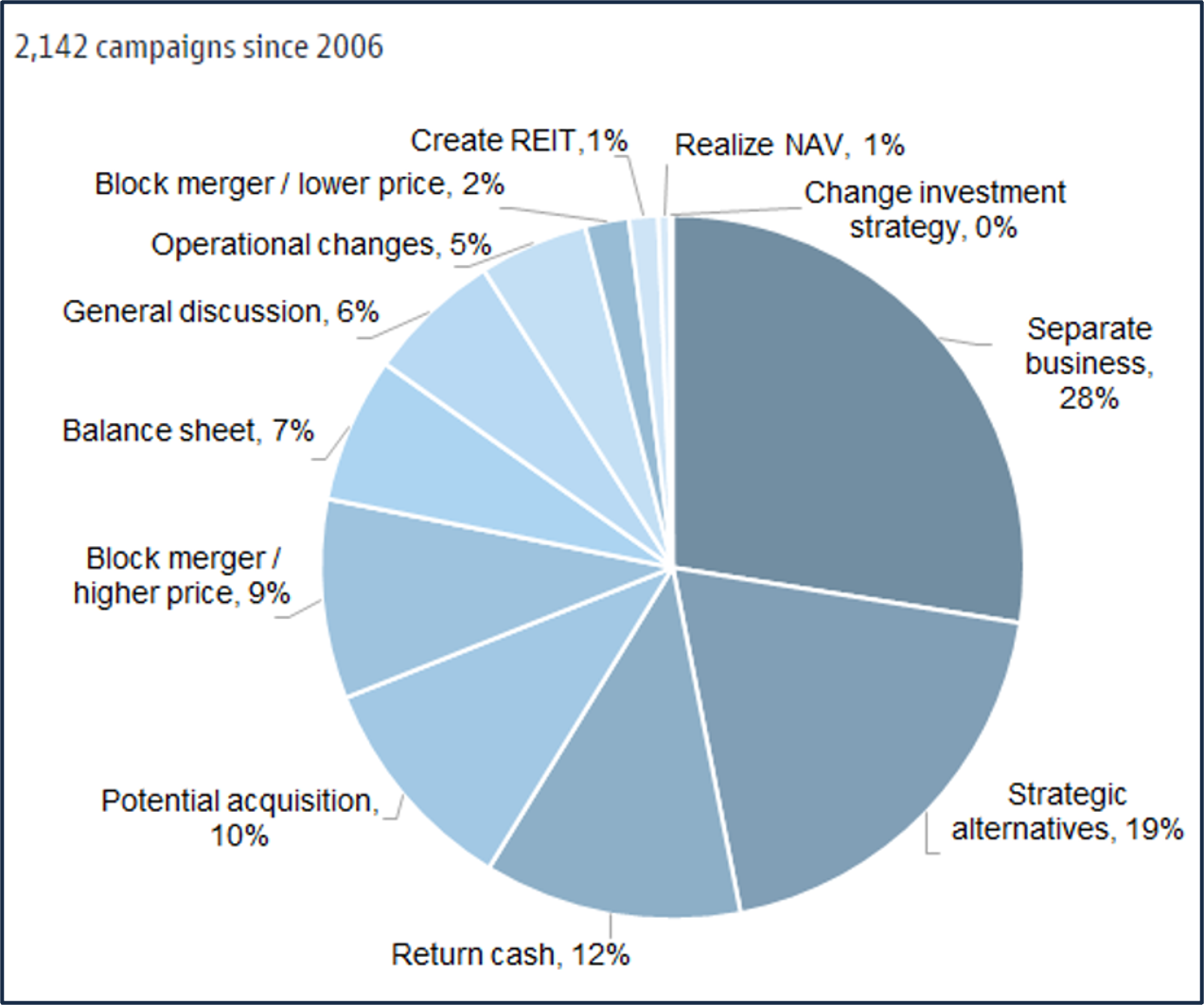

As the below graph shows, separating business units (i.e., a spinoff) is the most common value creation demand among activist shareholders (made in ~28% of activist campaigns from 2006 to 1Q 2023). As a result, we believe that activist campaigns have likely influenced spinoff performance due to how these investors have pressured companies to unlock value by divesting assets, which may have led management to spin off underperforming units or those not able to thrive on a standalone basis.

Value Creation Demands from Activist Investors

Source: FactSet, Goldman Sachs Global Investment Research.

Pruning corporate deadwood:

Even without shareholder pressure, we believe that more companies are spinning off dressed-up, underperforming units (sometimes as a defensive maneuver, to avoid becoming an activist target). Instead of investing in a flagging subsidiary, management stops spending any money on it whatsoever and sends it off on its own. This type of spinoff is generally good for the parent company but leaves the spinoff in a weakened state when it becomes an independent entity.

Weeding Out Underperformers

Although overall spinoff performance has been poor recently, there have been some bright spots. Outperforming spinoffs still exist; they might just take a little more digging to find. Our team’s analysis of spinoffs’ recent performance suggests some rules of thumb for investors who want to separate potential outperformers from the pack:

1. Embrace momentum:

Buying a stock after its price goes up is psychologically hard to do. With spinoffs, however, we’ve found that 1-year outperformers tend to keep posting strong performance compared with their peers, whereas 1-year underperformers tend to post more lackluster returns. Past performance doesn’t predict future results, but in the case of spinoffs, 1-year performance can be a valuable data point for separating the proverbial wheat from the chaff. For example, the spinoff featured in our upcoming opportunity report has outperformed the S&P 500 by over 700 bps (as of September 12, 2023) since it was spun out.

Source: Boyar Research Report, 2019.

These charts reveal that 1-year outperformers tended to continue posting strong performance versus the benchmark—returning, on average, 16% annualized excess on an inception-to-date basis (after delivering strong >20% annualized returns on a 3- and 5-year basis). Similarly, 1-year underperformers continued posting lackluster returns—returning, on average, -19% annualized excess on an inception-to-date basis. The trend that emerges from the data may be explained by the difference between spinoffs that emerge when the parent company divests a strong business that has growth potential and those that emerge when it divests underperforming units that have unattractive balance sheets and/or growth prospects.

2.Look for involuntary departures:

As already noted, spinoffs often underperform when companies get rid of business units that management perceives as dead weight. One way to avoid these situations is to look for spinoffs that the parent company’s management might not have wanted to lose. For example, government-mandated spinoffs stemming from antitrust regulations may signal the potential for good appreciation potential, since they can force a company to spin off an otherwise profitable part of its business.

3.Follow the parent company’s money:

Parent companies often retain a large stake in the firms they spin off. If a parent company holds onto its spinoff’s stock, management is likely very confident about the spinoff’s future. Similarly, when high-ranking corporate officers move to a spinoff’s C-suite or serve on its board, that can be a sign that someone in the know is confident about the spinoff’s prospects—after all, executive compensation is frequently linked to performance.

Stocks to Keep an Eye On

According to Kiplinger, in 2022 U.S. companies announced 44 spinoffs and completed 20, totaling $61 billion in market value. Through mid-July of this year, nine U.S. spinoffs have been completed.

Our analyst team has been hard at work analyzing some of these opportunities, trying to separate the trash from the treasure. In the April issue of Asset Analysis Focus, we highlighted GE’s divestiture of GE Health Care (which fits many of the criteria of potentially successful spinoffs, as GE kept a substantial stake in GE Healthcare and top management stayed with the spun-off entity), but thus far GE Health Care has trailed the broad market in terms of stock price performance.

In May of this year, Asset Analysis Focus also profiled the separation of MSG Sphere from Madison Square Garden Entertainment in our report on MSGE and the MSG Sphere.

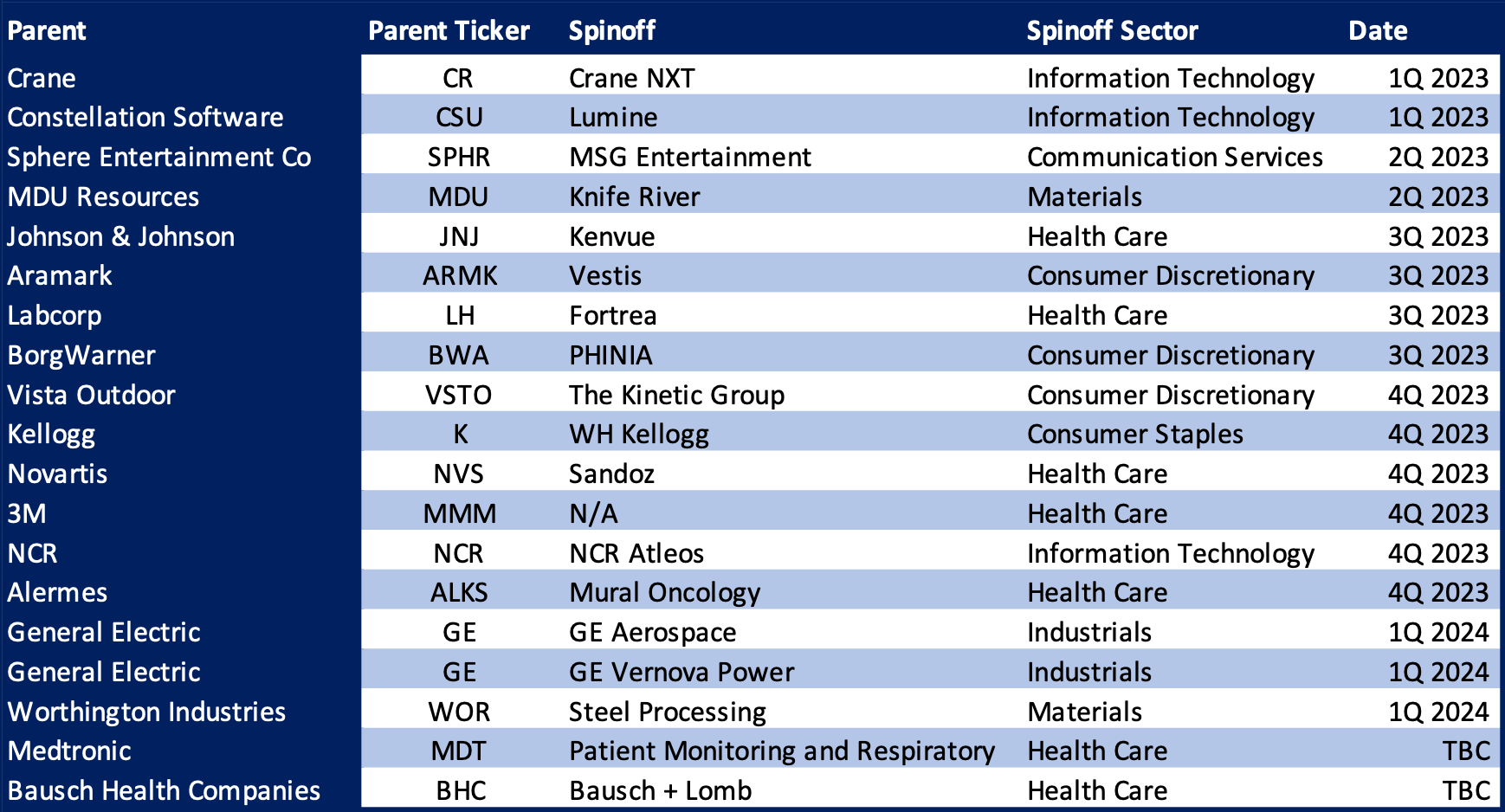

2023 has been a somewhat active year for spinoffs, and here at Boyar Research, we’ll be profiling the ones that we think exhibit the greatest risk/reward characteristics. Additionally, the following companies have spun off in 2023 or are scheduled to do so in the near future. We are not predicting that any of these particular names will be winners, but they are certainly worth keeping an eye on.

Important Disclosures. The information herein is provided by Boyar’s Intrinsic Value Research LLC (“Boyar Research”) and: (a) is for general, informational purposes only; (b) is not tailored to the specific investment needs of any specific person or entity; and (c) should not be construed as investment advice. Boyar Research does not offer investment advisory services and is not an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) or any other regulatory body. Any opinions expressed herein represent current opinions of Boyar Research only, and no representation is made with respect to the accuracy, completeness or timeliness of the information herein. Boyar Research assumes no obligation to update or revise such information. In addition, certain information herein has been provided by and/or is based on third party sources, and, although Boyar Research believes this information to be reliable, Boyar Research has not independently verified such information and is not responsible for third-party errors. You should not assume that any investment discussed herein will be profitable or that any investment decisions in the future will be profitable. Investing in securities involves risk, including the possible loss of principal. Important Information: Past performance does not guarantee future results.

This information is not a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, including an interest in any investment vehicle managed or advised by affiliates of Boyar Research. Any information that may be considered advice concerning a federal tax issue is not intended to be used, and cannot be used, for the purposes of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter discussed herein. Clients of an affiliate of Boyar Research and employees of Boyar Research own shares in GE Health Care, Madison Square Garden Entertainment, MSG Sphere. Johnson & Johnson, LabCorp, Fortrea & Medtronic.