Topgolf Update: Our Meeting with CEO Chip Brewer

Topgolf Update: Our Meeting with CEO Chip Brewer

TopGolf Callaway Brands Corp. (MODG)

Topgolf reported its 3Q 2023 results earlier this month. Key components of the earnings release were that overall revenues and adjusted EBITDA increased by 5.1% (slightly below consensus estimates) and 13.1% (well above consensus estimates), respectively on a year over year basis for the quarter. Results were aided by the Topgolf segment, which accounts for about half of the Company’s overall profitability, where revenues and adjusted EBITDA increased by 8.2% and 42%, respectively.

So why did the shares decline by 17% in the wake of these solid results?

Our analyst team spoke with CEO Brewer after earnings were released to find out more. We then revisited our thesis in the company to see if the share price decline is a buying opportunity or were we simply wrong in our initial assessment of TopGolf’s prospects.

We attribute the adverse share price reaction in the wake of the results (note: shares have retraced a good portion of their losses following the disclosure that a number of key insiders, including the CEO, have purchased shares following the earnings release) to investor scrutiny of Topgolf’s same venue sales (SVS), which disappointed for the quarter (down 3% vs. management’s outlook calling for growth of 1-3%) and whose full year outlook was reduced for the second time this year (to down slightly % vs. a prior outlook of up mid-to-high single digit %, and an initial 2023 outlook calling for high single-digit % growth).

Since Topgolf is rapidly growing through the opening of new venues, SVS allows a comparison of how the sales of venues that have already been established in the market for a period of time compared with the year-ago quarter. The disappointing results on the SVS front largely stem from pressure within corporate business, which accounts for ~20% of Topgolf segment revenues. In reducing their estimate for SVS in May 2023, management attributed the decline to weakness it was seeing in Topgolf’s corporate business in the wake of the banking crisis. When we followed up with management after the 3Q 2023 earnings report, they admitted that they overestimated the permanence of the post-covid/omicron surge in corporate business (illustrated in the graphic below) (i.e. much of that growth was attributed to events/gatherings that proved to be one-time in nature).

While it seems like the confluence of adverse events suggest the sky is falling, we believe they are just a hiccup in the Company’s growth trajectory, which continues to look strong.

Although the SVS trends are worth monitoring, we don’t believe that they reflect the longer-term prospects of the business. Rather, we believe they represent the difficulties of operating in a post-covid environment that have created difficult quarter-over-quarter comparisons coupled with some softness in economic activity in the wake of unprecedented interest rate increases over the past ~18 months. Although there are some investors (who have a much shorter time horizon then we do) that have voted with their feet based on concern that the Topgolf entertainment concept could be a fad, we would note that during our recent conversation with management, it was highlighted that there are venues in the UK that were opened some 15 years ago that have been delivering low to mid-single digit SVS growth in recent years. This is critically important as one of the concerns among investors is that TopGolf is a fad and does not have the growth opportunities the company projects. The fact that locations that have been in operation for 1.5 decades are still experiencing growth helps to rebut that thesis. Moreover, recent management actions earlier this month suggest that management is not concerned in the outlook for the Topgolf entertainment concept when they acquired certain venues from BigShots, its largest active competitor. It should also be noted that a number of key insiders have bought shares on the open market in the wake of the earnings sell off, including CEO Chip Brewer who deployed ~$350k in the purchase of 35k shares (average price: ~$10 a share).

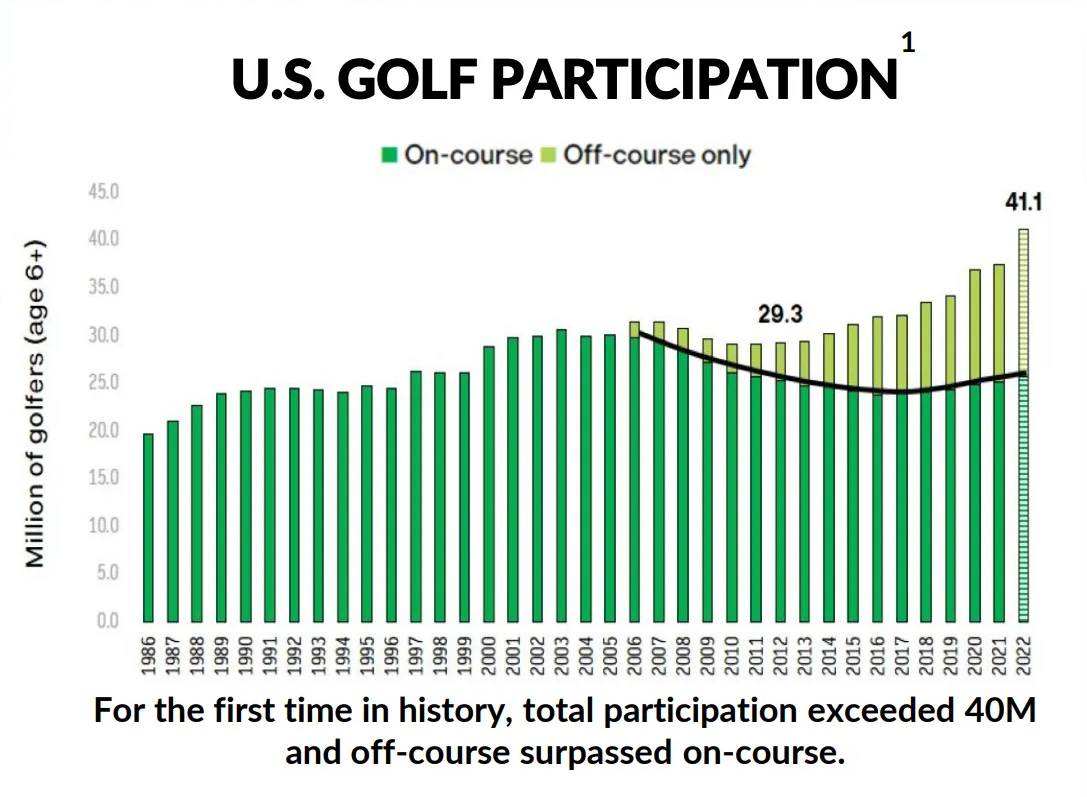

As the father of value investing Benjamin Graham stated, “in the short run the market is a voting machine but in the long term it is a weighing machine.” We believe that statement is an accurate characterization of Topgolf’s recent share price performance. Shares have been cut in half this year as investors have fretted over the Company’s near term SVS performance. Management also recently pushed out their forecast for company-wide adjusted EBITDA of over $800 million to 2026 from 2025 primarily due to adverse foreign currency movements from the time it originally communicated its long-term outlook in 2022. The addressable market for new venues domestically and internationally is massive and the game of golf has seen a rebound/surge in both on and off course golfers (see graphic below), which should provide a nice tailwind for MODG’s various businesses for years to come.

Activist Investor?

It would not surprise us if Topgolf caught the attention of an activist investor. While we understand the strategic rationale for owning Travis Matthews, we view Jack Wolfskin as non-core. Jack Wolfskin is generating roughly the same amount of EBITDA (~20 million euros) today as when they bought the company in 2019. They believe this could be a 70 million euro adjusted EBITDA business by 2025. If they were able to sell the business and utilize the proceeds to pay down debt and/or buyback stock, we believe the stock would react quite favorably.

Valuation

With the sell-off post earnings, MODG shares look incredibly cheap trading at just ~7.3x on an EV/2023E EBITDA. It should be noted that golf equipment industry peer Acushnet currently trades at ~13x on an EV/EBITDA basis. Meanwhile, Taylor Made was acquired for approximate mid-teens EV/EBITDA multiple. Applying a discounted 11x multiple to the Company’s 2023E EBITDA produces a valuation of $22 a share, or ~110% upside from current levels. We believe the Company’s 2023E profitability (2023E EBITDA: $580 million), significantly understates future levels of profitability with management targeting over $800 million in EBITDA by 2026 (previously targeted for 2025).

Important Disclosures. The information herein is provided by Boyar’s Intrinsic Value Research LLC (“Boyar Research”) and: (a) is for general, informational purposes only; (b) is not tailored to the specific investment needs of any specific person or entity; and (c) should not be construed as investment advice. Boyar Research does not offer investment advisory services and is not an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) or any other regulatory body. Any opinions expressed herein represent current opinions of Boyar Research only, and no representation is made with respect to the accuracy, completeness or timeliness of the information herein. Boyar Research assumes no obligation to update or revise such information. In addition, certain information herein has been provided by and/or is based on third party sources, and, although Boyar Research believes this information to be reliable, Boyar Research has not independently verified such information and is not responsible for third-party errors. You should not assume that any investment discussed herein will be profitable or that any investment decisions in the future will be profitable. Investing in securities involves risk, including the possible loss of principal. Important Information: Past performance does not guarantee future results.

This information is not a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, including an interest in any investment vehicle managed or advised by affiliates of Boyar Research. Any information that may be considered advice concerning a federal tax issue is not intended to be used, and cannot be used, for the purposes of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter discussed herein. Clients of an affiliate of Boyar Research and employees of Boyar Research own shares in Topgolf Callaway Brands Corp.