July's Opportunity: The Howard Hughes Corporation

Why hedge fund titan Bill Ackman has been buying millions of dollars of HHC a day—and why we believe investors should follow his lead

A Foreword by Jonathan Boyar:

At Boyar Research, we never stop searching for hidden value in the stock market, and for nearly 50 years, we’ve found that real estate is one of the best places to uncover it. I’m reminded of a story my father, Mark (the founder of Boyar Research), has been telling since I was a kid: every morning on his way to work in 1975, he walked by Tiffany & Co.’s flagship store on Fifth Avenue and 57th Street. He knew that Tiffany owned iconic brands, but he wondered whether the company also owned this valuable Manhattan trophy property. His research (which was much more difficult to do in the 1970s than in today’s digital age) revealed that not only did the company indeed own the real estate, but the market value of Tiffany’s itself was less than that of the company’s owned real estate. In short, investors who bought Tiffany Stock in 1975 got the whole business—the Tiffany trademark, its inventory, even the world-famous Tiffany Diamond—for free! Tiffany was one of the first stocks Boyar Research ever profiled. Just 3 years later, Tiffany & Co. was acquired by Avon Products at a price 450% higher than when we initially profiled it.

Boyar Research reports, circa 1975 and 1978.

Such discrepancies are not merely a relic of decades past. Over the years, we’ve seen Wall Street undervalue one company after another when analysts have overlooked the value of the underlying real estate. For example, during the Great Financial Crisis, Saks Fifth Avenue Enterprises shares were trading for less than the real estate the company owned on Fifth Avenue. A few years later it was bought by Toronto-based Hudson’s Bay Company for $2.4 billion.

Howard Hughes Corp.

NYSE: HHC

Editors note: On August 14, 2023, Howard Hughes Corp. changed its name and stock symbol. The Company is now Howard Hughes Holdings (HHH).

Getting the Lay of the Land

“Buy land,” Mark Twain used to say: “They’re not making it any more.” Howard Hughes Jr., the renowned film producer, aviator, and business magnate, took this to heart when he acquired a massive parcel—25,000 acres—of raw land on the outskirts of Las Vegas in 1952 . . . for just $3 an acre. Some of this very same land is now being sold for residential and commercial development for around $1,100,000 an acre—talk about appreciation!

Today, the Howard Hughes Corporation (named in honor of the late renaissance man’s legacy) owns this valuable Las Vegas real estate, which has been under development for the last three decades or so as part of the Summerlin master-planned community (MPC).

MPCs are large, mixed-use residential neighborhoods whose curated amenities (parks, hiking trails, playgrounds, pools, golf courses, tennis and basketball courts, etc.) and commercial opportunities make them the perfect place for people to live, work, and play.

MPC Amenities

Unlocking the Potential of Property

Why are situations involving real estate often so ripe with opportunity? Because reported book value (what a company values an asset for on its balance sheet) can be far below a company’s actual market value. Accounting conventions aren’t good at reflecting the market value of land or buildings—which often appreciate in value over time—since they do not allow for increases in value on a company’s balance sheet. These assets must be valued at what they were purchased for (even if that purchase happened 100 years ago!). For these reasons, investors who simply rely on the balance sheet to assess the value of a company often incorrectly value real estate assets, but those who do their homework—and who are willing to be patient—can make sizable gains.

The Business

HHC’s Real Estate Portfolio across the Country

Building Communities for the Future

The Las Vegas Summerlin community is just one development in the Company’s impressive roster of assets. Howard Hughes owns land and commercial real estate across the country, mostly (but not entirely) consisting of large-scale MPCs in Nevada, Texas, Maryland, and Arizona. Within these sprawling oases, the Company owns, develops, and operates top-quality commercial real estate that suits a variety of needs, from multifamily and office uses to retail and hospitality.

A Glimpse of the MPCs

Howard Hughes enjoys distinct competitive advantages within these MPCs. Since the Company controls the supply of new construction, it does not have to worry about major disruptions from commercial development competitors and it maintains pricing power over leasing arrangements. The Company often touts its “virtuous cycle” of value creation: as it sells land to homebuilders, population growth increases the demand for nearby income-producing commercial real estate, which the Company then develops—increasing the value of its remaining land.

Self-Funded Business Model

For those who enjoy a sea view, the Company also develops and sells premier condominiums in Ward Village, a development along the Hawaiian coastline, adjacent to downtown Honolulu. In this “vertical MPC,” high-end condo units are sold to individual buyers, typically at a 25%-30% gross profit margin. The cash generated from condo closings is generally earmarked for reinvestment into other development opportunities, including additional Hawaiian condo developments.

Ward Village/Condo Tower

Finally, HHC owns an array of assets in the city blocks around downtown Manhattan’s Pier 17, where it acts as a landlord, manages businesses, and even hosts outdoor events. In 2012, Superstorm Sandy ravaged the Seaport, and since then the Company has been redeveloping the district to make it much more weather-resilient. (Underground utilities are housed in submarine hulls, and building structures on the pier have been elevated above the floodplain.) The Seaport has been the financial laggard of the group but seems to be turning a corner, with post-COVID foot traffic to the area increasing in conjunction with concert venue and restaurant reopenings.

The Seaport

The Financials

Building a Cash-Flow Machine, One Asset at a Time

Net Operating Income (NOI) is a key statistic used by real estate investors. It is the revenue generated from a property, such as rent (after deducting for expected vacancies and credit losses), minus operating expenses (consisting of maintenance, insurance, property-level taxes, and other overhead). NOI excludes things that are affected depending on the owner (e.g., interest expenses and income taxes) and therefore provides a clearer financial picture of the property itself.

Howard Hughes has a real estate portfolio that is set to deliver an increasing, largely recurring income stream. In 2022, its portfolio of high-quality operating assets (office buildings, multifamily housing, retail space, and miscellaneous other properties) generated net operating income (NOI) of $239 million, up 9% (excluding dispositions) from the previous year. As of the first quarter of 2023, annualized NOI from in-place tenants remained $239 million:

NOI Breakdown by Asset Type (MM)

The Company’s NOI growth has been remarkable: back in 2011, the Company was generating just $46 million from its commercial property operations. These noteworthy gains are thanks to the completion of various construction projects, which generate largely recurring revenue through rent collections once they are placed into service.

Robust Operating Assets NOI Growth ($MM)

We don’t expect the growth trajectory to stop any time soon. Income from these high-end properties goes right back into self-funding extensive developments within the Company’s MPCs and other properties. A development horizon spanning years and even decades from now will dramatically increase the Company’s income streams over time.

At present, five additional construction projects are under way (four of which commenced in 2022), which should collectively add $20 million to annual operating income once stabilized between 2026 and 2028. Rental rate increases should also keep driving higher operating results.

Even against today’s discouraging office backdrop, HHC’s office rental rates are climbing (+11% same-location office rent in the first quarter). Why the disparity? Because HHC’s office portfolio largely comprises high-quality and relatively new buildings (average age 12 years) that are located in in-demand areas and surrounded by an abundance of amenities. Older and outdated office buildings are having a hard time attracting and retaining tenants as demand has shifted toward better-quality offices, which are viewed in a far more favorable light by corporate occupiers and the employees who still spend their 9 to 5 in an office.

Affluent Markets and Favorable Migration Trends

Today the Howard Hughes portfolio includes prime U.S. real estate in upscale regional markets across the nation. While it operates in six states, it is concentrated mainly in low-tax, business-friendly states with desirable weather. Several high-profile companies have made headlines by electing to depart from high-tax jurisdictions like California in recent years, relocating jobs to Texas or other such states.

State Income Tax Rates in HHC States vs. California

Similarly, the pronounced housing affordability crunch—a combination of lofty property values and higher mortgage rates—should keep nudging homebuyers to seek better value propositions around the country, where newcomers have greater purchasing power. And given the proliferation of remote work, more Americans are able to uproot and relocate in new states than ever before. Some of the Company’s most significant exposure is to markets benefiting from strong in-migration trends, particularly Houston and Las Vegas, which were the respective #1 and #2 moving destinations in both 2021 and 2022, according to Penske Corporation.

HHC Is Supporting Housing Supply in Critical Regions (NV, AZ, TX)

A Shortage of Housing, Not of Opportunity

Ever since the Great Financial Crisis, which was spurred largely by a glut of housing supply and ridiculously loose lending practices, overly conservative homebuilders have not kept up with the rise in household formations. The COVID-19 outbreak revealed this stark contrast when the exodus from densely populated cities to the suburbs resulted in highly imbalanced supply and demand, even as new housing construction activity was stifled by a lack of labor and elevated costs for lumber and other materials.

Nowadays, most homeowners have locked in historically low mortgage rates, making them reluctant to sell their houses. As a result, the National Association of Homebuilders estimates that 33% of for-sale homes are new construction rather than existing construction, versus just 10% normally.

The recent surge in interest rates affected the pace of housing starts (the beginning of construction of new houses) in late 2022 and early 2023. However, homebuilders are realizing that with a dearth of existing homes for sale on the market, demand for new homes remains high. HHC works with over a dozen homebuilder companies that buy land lots within the MPCs. Homebuilder land inventory levels are low and need to be replenished, which should lead to increased land parcel sales volume in the coming quarters.

Not only is the nation facing a housing undersupply of anywhere from 4 to 5 million homes, but Phoenix alone (one of the top 5 U.S. metropolitan in-migration areas) is said to account for 600,000 of that shortfall. It’s no surprise, then, that property values in the area have skyrocketed since the pandemic. The Company’s newest MPC—the fledgling Teravalis—is located on the western outskirts of Phoenix and is mostly just raw land at this stage. HHC acquired the 37,000-acre swath of land for $600 million in 2021. Teravalis is gearing up to contract out the new community’s first 1,000 homes (of an eventual 100,000 households) in the back half of this year. While reaping the rewards of this brand-new development will require patience, the amount of value it can add for shareholders over a long period is enormous: remember how the Las Vegas land, once worth $3, per acre has eclipsed $1 million an acre (admittedly, an extreme example).

Teravalis

The Stock

A Hedge Fund Titan’s Big Bet

We’re not alone in our opinion of Howard Hughes Corporation’s undervaluation and massive long-term potential. Well-known hedge fund manager Bill Ackman, the CEO of hedge fund Pershing Square Capital Management, chairs HHC’s board and owns a huge stake in the Company.

Since late last year, perceiving a steep undervaluation of the shares, he’s been voraciously acquiring more stock, upping his ownership interest from 27% to 33%, now worth about $1.3 billion. Last year, Ackman initiated a tender offer—a public bid to buy large quantities of stock from existing shareholders—for up to $70 a share. However, existing investors were hesitant to sell their shares, signifying their belief that the stock is worth much more than that. More recently, Pershing Square has been systematically acquiring HHC stock on the open market (sometimes millions of dollars’ worth a day) at prices up to $75 per share, providing strong price support around that level.

Because of his position as chairman, Bill Ackman has access to far better information than just about anyone else regarding the Company’s prospects and the stock’s discount to intrinsic value. We consider his buying activity to be a huge vote of confidence in the business and a bullish indicator for other investors.

The Company, too, has been active in the market for HHC stock. In 2022, Howard Hughes reduced its outstanding share count by about 8% by buying back $400 million of its stock. Management didn’t mince words, describing repurchases at $89 a share as being made “well below intrinsic value”—certainly a compelling recommendation. (And today investors are able to buy HHC at an even more attractive entry point.)

A Different Kind of Real Estate Investment

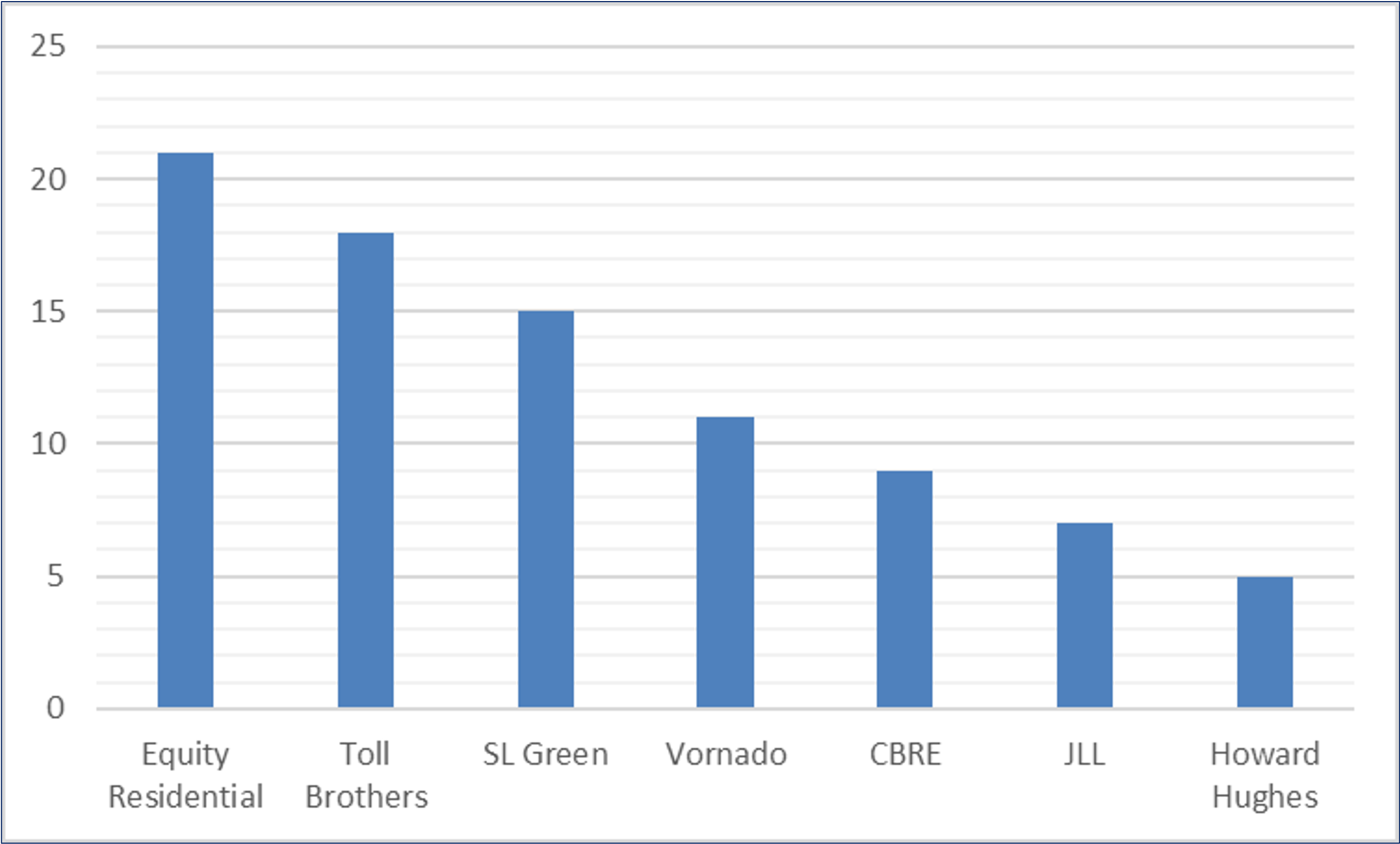

You’d think a company that inspires such enthusiasm among its shareholders and management would draw attention from all sides, but HHC is barely a blip on Wall Street’s radar. The portfolio of MPCs is unique for a publicly listed entity, and HHC’s habit of reinvesting capital instead of distributing it through dividends makes it distinctly different from its more widely followed REIT (real estate investment trust) peers, which are required to pay out ≥90% of earnings as dividends. The Company’s ability to retain earnings for development enhances its growth prospects, yet these unusual characteristics make HHC underfollowed for a company of its scale, leaving it as an “orphaned” stock, with just five Wall Street analysts covering it versus a dozen or more for its mid- to large-cap real estate peers.

Analyst Coverage of Select Real Estate Companies

Primed for Gains

Howard Hughes has grown its income-producing asset base at an impressive clip. At just $77 per share, the stock is actually cheaper than it was in 2013, yet over that 10-year span, NOI from operating assets has surged more than fourfold, to $239 million. Plus, HHC is poised to be a compounding machine for decades to come, taking advantage of the massive development runway within its already owned communities.

Meanwhile, though the business has weathered the stormclouds of higher interest rates, its shares have dropped 25% over the past 12 months. However, weather-beaten short-term-focused sellers are overlooking something: value.

We strongly believe that the Company’s collection of properties is worth far more than its current stock price. Public market investors often have trouble ascribing appropriate value for non-income-producing assets, like land (which makes up a significant portion of HHC’s overall value)—which may be part of why HHC is trading at a sizable discount to its intrinsic value. Erring on the side of caution and using what we consider to be extremely conservative real estate valuation assumptions, we estimate that the Company’s intrinsic value is at least $104 a share today, roughly 35% above the recent stock price.

In our opinion, HHC holds significant appeal for growth and value investors alike.

Important Disclosures. The information herein is provided by Boyar’s Intrinsic Value Research LLC (“Boyar Research”) and: (a) is for general, informational purposes only; (b) is not tailored to the specific investment needs of any specific person or entity; and (c) should not be construed as investment advice. Boyar Research does not offer investment advisory services and is not an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) or any other regulatory body. Any opinions expressed herein represent current opinions of Boyar Research only, and no representation is made with respect to the accuracy, completeness or timeliness of the information herein. Boyar Research assumes no obligation to update or revise such information. In addition, certain information herein has been provided by and/or is based on third party sources, and, although Boyar Research believes this information to be reliable, Boyar Research has not independently verified such information and is not responsible for third-party errors. You should not assume that any investment discussed herein will be profitable or that any investment decisions in the future will be profitable. Investing in securities involves risk, including the possible loss of principal. Important Information: Past performance does not guarantee future results.

This information is not a recommendation, or an offer to sell, or a solicitation of any offer to buy, an interest in any security, including an interest in any investment vehicle managed or advised by affiliates of Boyar Research. Any information that may be considered advice concerning a federal tax issue is not intended to be used, and cannot be used, for the purposes of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter discussed herein. Clients of an affiliate of Boyar Research and employees of Boyar Research own shares in Howard Hughes Corporation.